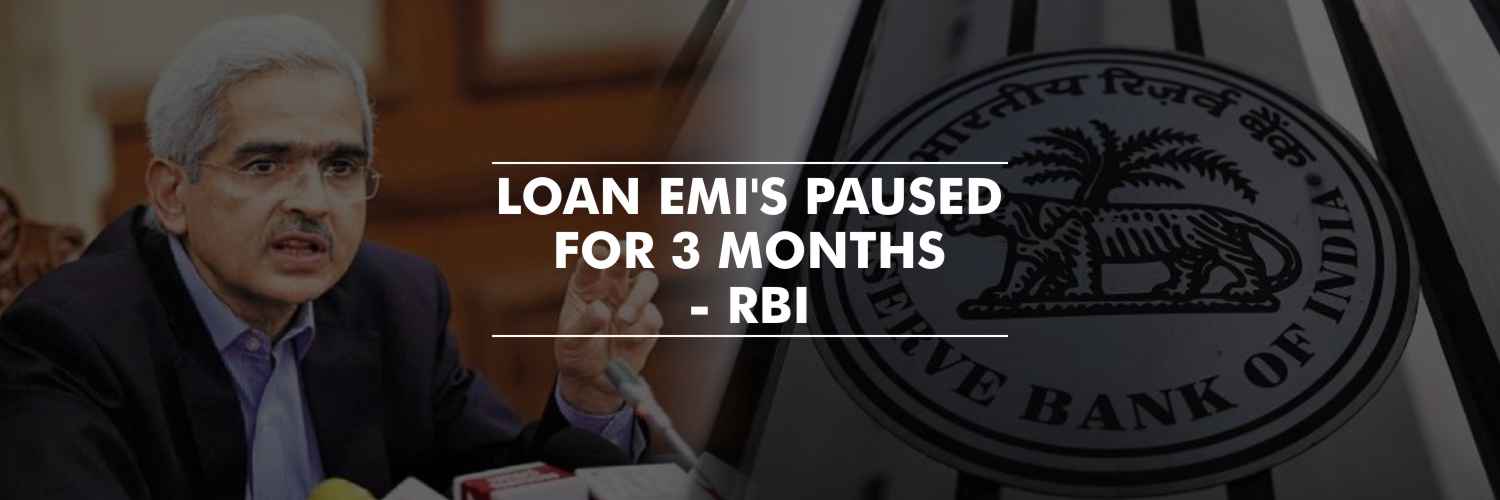

Amid the ongoing COVID-19 crisis, which had a serious impact on various sectors including businesses and employees in India, the Reserve Bank of India in a press conference on Friday, announced that all banks and NBFCs have been permitted to allow a moratorium of 3 months on repayment of all kinds of loans outstanding on 1 March 2020. Evidently, the 3 months moratorium on repayment of term loans by borrowers means, that they would not have to pay the loan EMI installments during the moratorium period.

“All commercial banks (including regional rural banks, small finance banks and local area banks), co-operative banks, all -India Financial Institutions, and NBFCs (including housing finance companies and micro-finance institutions) (lending institutions) are being permitted to allow a moratorium of three months on payment of installments in respect of all term loans outstanding as on March 1, 2020. Accordingly, the repayment schedule and all subsequent due dates, as also the tenor for such loans, maybe shifted across the board by three months” stated RBI Governor Shaktikanta Das.

This implies that individuals’ EMI repayments of loans taken, would not be deducted from their bank accounts till the moratorium period is over, which will restart only once the moratorium period of 3 months expires.

The RBI further clarified that availing the moratorium will neither entails any financial penalties or increase in the interest rate or charges beyond the existing terms and conditions of the loan nor would it lead to a downgrading of the borrower’s credit rating or affect the risk classification of the loan.

Additionally, all lending institutions and banks have been allowed to defer interest on working capital repayments by three months and further allowed banks to reassess the working capital cycle stating that they won’t be treated as non-performing assets.

Naturally, if the loan repayment is deferred then the borrower’s credit history and risk classification of the loan can be adversely impacted. However, as per the RBI statement, in the case of this moratorium, the borrower’s credit rating will not be impacted in any way.

As per Reserve Bank of India (RBI) rules, any default payments have to be recognized within 30 days and these accounts are to be classified as special mention accounts.

RBI’s Monetary Policy Committee (MPC), also decided to cut the repo rate by 75 basis points to 4.4 percent, while the reverse repo rate has been reduced by 90 basis points. Citing the current crisis as “extraordinary circumstances”, the RBI Governor stated that the MPC voted for a sizeable reduction in repo rate to revive growth, mitigate COVID-19 impact.

“The rescheduling of payments will not qualify as a default for supervisory reporting and reporting to Credit Information Companies (CICs) by the lending institutions. CICs shall ensure that the actions taken by lending institutions pursuant to the above announcements do not adversely impact the credit history of the beneficiaries,” read the RBI statement.

The Central bank governor further asserted that “The moratorium/deferment is being provided specifically to enable the borrowers to tide over the economic fallout from the pandemic. Hence, the same will not be treated as a change in terms and conditions of loan agreements due to the financial difficulty of the borrowers and, consequently, will not result in asset classification downgrade.”

The RBI governor has also pushed for more liquidity in the system to help banks increase liquidity to help businesses when the lockdown is removed.

“A multi-pronged approach, comprising both targeted and system-wide liquidity provision, has been adopted to ensure that COVID-19 related liquidity constraints are eased. Liquidity availed under the scheme by banks has to be deployed in investment-grade corporate bonds, commercial paper, and non-convertible debentures over and above the outstanding level of their investments in these bonds as on March 25, 2020. Eligible instruments comprise both primary market issuances and secondary market purchases, including from mutual funds and non-banking finance companies,” stated the governor.

As per sources, this decision by the central bank came after the Finance Ministry wrote to the bank seeking a moratorium on EMI, interest and loan repayments for a few months, as there have been various requests from stakeholders to defer the EMI payments as the country is going through a 21-day lockdown, due to detrimental spread of COVID-19.

The current decisions taken by the RBI would provide a big relief to the individuals, especially the self-employed, businesses facing a big economic challenge due to loss of income during the 21-day lockdown period, in view of the pandemic disease.

Earlier, on 26 March, Finance Minister Nirmala Sitharaman on Thursday announced a relief package worth Rs 1.70 lakh crore for various sectors of the nation, to tackle financial difficulties arising from the ongoing Coronavirus crisis. The scheme is likely to focus on economic relief primarily to migrant laborers and daily wage laborers, which includes a mix of food security and direct cash transfer benefits to the poor families during the lockdown.

On 24 March, FM Sitharaman has extended the last date to file Income Tax and Goods and Services (GST) returns and Aadhaar-PAN linkage to file IT returns, to 30 June.